AI Debt Binge: Taiwan's $14.5B Bet on Future Capacity

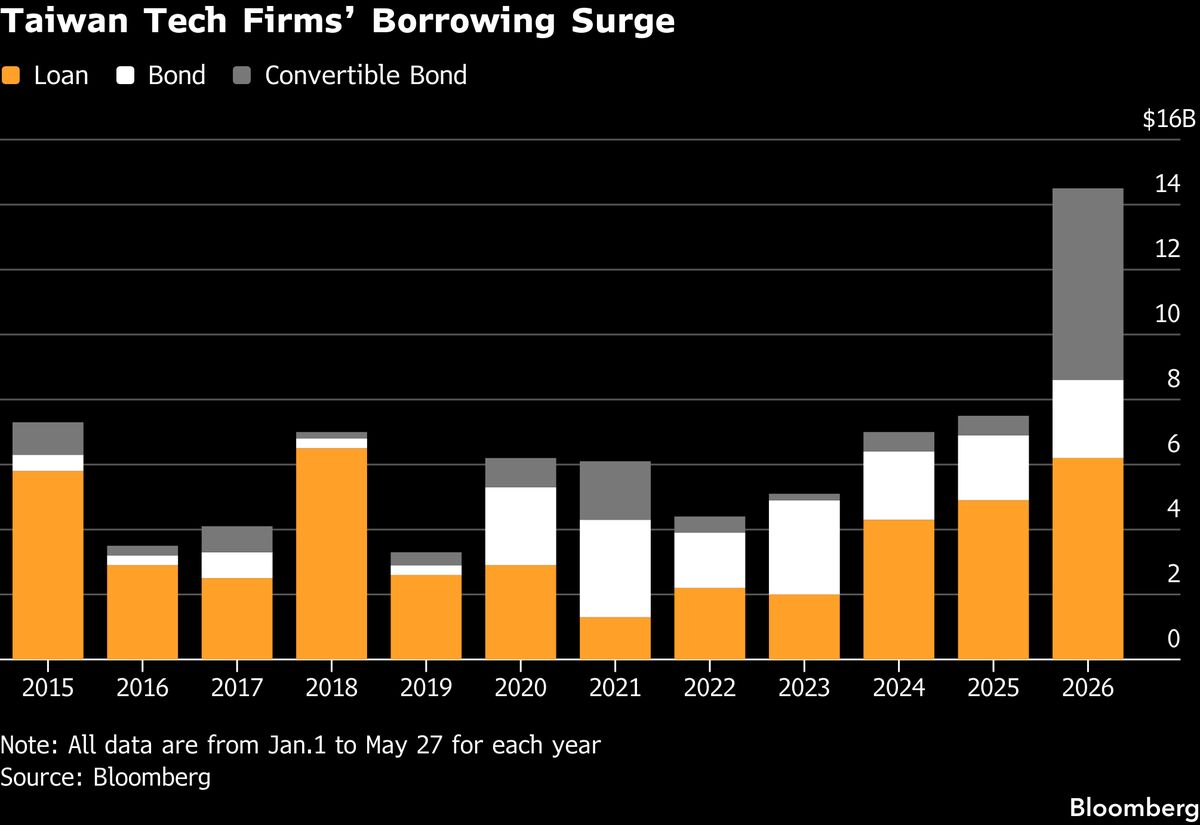

Taiwanese tech firms have raised $14.5 billion in debt deals so far in 2026, the highest ever, driven by AI infrastructure demand. This borrowing spree reveals a market splitting between those who can afford to build and those who are borrowing to survive.

Taiwanese tech firms just borrowed a record $14.5 billion in debt this year, according to Bloomberg. This is not a sign of health — it is a desperate race to lock in financing before interest rates rise further and AI demand potentially cools. The winners and losers are already separating.

- Taiwanese tech firms completed $14.5 billion in debt deals in 2026, a record driven by AI capacity demand.

- TSMC and its direct suppliers are the primary borrowers, using debt to fund advanced packaging and fab expansions.

- The borrowing spree creates a two-tier market: well-capitalized leaders vs. over-leveraged followers.

- This article explains who wins, who loses, and what happens when the AI capex cycle slows.

Why Did Taiwanese Tech Firms Borrow $14.5 Billion in 2026?

According to Bloomberg, Taiwanese technology companies have completed a record $14.5 billion of debt deals so far in 2026, as they race to secure financing for AI capacity. The borrowing is concentrated among semiconductor manufacturers and their equipment suppliers. TSMC alone has issued over $6 billion in bonds this year, according to Bloomberg data, primarily to fund its advanced packaging capacity for Nvidia and AMD AI chips. The urgency is clear: AI chip demand is outstripping supply, and any delay in capacity expansion means lost revenue to competitors like Samsung and Intel.

Is This Borrowing Spree Sustainable or a Bubble?

The short answer is no, not for everyone. Bloomberg reported that the debt deals are being absorbed by institutional investors hungry for yield, but the underlying risk is rising. The borrowing is concentrated in a few large firms — TSMC, MediaTek, and Quanta Computer — while smaller players are being shut out of the bond market or paying punitive rates. According to a Bloomberg Intelligence analyst quoted in the article, the average coupon on Taiwanese tech bonds has risen 80 basis points since 2024, indicating that lenders are demanding higher compensation for what they perceive as growing risk. The market is already pricing in a bifurcation: TSMC can borrow at near-risk-free rates, while second-tier firms pay a premium that erodes their margins.

Who Actually Benefits From This Debt-Fueled Expansion?

The clear winners are TSMC and its direct equipment suppliers, such as ASML and Tokyo Electron. According to Bloomberg's analysis, TSMC's debt-to-equity ratio remains below 30%, giving it ample headroom to service its new bonds. The company's AI-related revenue is expected to grow 40% in 2026, according to its own guidance, making the borrowing a rational bet. The losers are smaller Taiwanese fabless chip firms and second-tier foundries like UMC and Vanguard International Semiconductor. These companies are borrowing to keep up, but their AI exposure is lower, and their margins are thinner. When the AI capex cycle eventually slows — likely in 2028, based on historical semiconductor cycles — these firms will be left servicing debt on underutilized factories.

| Company | Debt Issuance (2026 est.) | AI Revenue Exposure | Debt-to-Equity Ratio | Verdict |

|---|---|---|---|---|

| TSMC | $6B+ | 45% | 28% | Winner — low risk, high return |

| MediaTek | $2B | 20% | 35% | Neutral — moderate AI exposure, manageable debt |

| Quanta Computer | $1.5B | 30% | 40% | Neutral — AI server demand supports borrowing |

| UMC | $1B | 10% | 45% | Loser — high debt, low AI revenue |

| Vanguard International | $0.5B | 5% | 50% | Loser — over-leveraged on non-AI capacity |

| Verdict: TSMC and its direct AI supply chain are clear winners; smaller foundries and fabless firms will struggle when the cycle turns. | ||||

What Does This Mean for Global AI Chip Supply?

The $14.5 billion borrowing binge directly funds the advanced packaging and 3nm/2nm capacity that Nvidia, AMD, and Google need for their next-generation AI accelerators. According to Bloomberg, TSMC's CoWoS (Chip-on-Wafer-on-Substrate) capacity will double by the end of 2026, enabling higher throughput for Nvidia's Blackwell and Rubin architectures. This means that AI chip supply constraints, which have been the primary bottleneck for data center buildouts, will ease in the second half of 2026. However, the debt-fueled expansion also means that any demand shock — such as a slowdown in enterprise AI adoption or a regulatory crackdown on data center energy use — would leave Taiwanese banks exposed to bad loans. Bloomberg reported that Taiwan's bank exposure to the tech sector has risen to 18% of total lending, up from 14% in 2024, a concentration risk that regulators are monitoring.

My thesis: Taiwan's $14.5 billion debt spree is a rational but dangerous bet that AI demand will remain insatiable for at least three more years. In the short term, the borrowing is necessary — TSMC and its suppliers cannot afford to underinvest while Intel and Samsung are pouring billions into foundry capacity. The long-term risk is that the AI capex cycle peaks in 2028, leaving over-leveraged firms with empty fabs and expensive debt. The clear winner is TSMC, which can service its debt from AI revenue alone. The losers are smaller Taiwanese foundries and fabless firms that are borrowing to keep up but lack the AI revenue to justify it. My prediction: by Q2 2028, at least two Taiwanese semiconductor firms will restructure their debt or seek government bailouts after the AI capex cycle peaks.

- By Q4 2027, TSMC will issue an additional $8 billion in bonds to fund its 1.4nm fab in Arizona, as U.S. AI demand forces onshore capacity expansion.

- By Q1 2028, UMC will announce a debt restructuring after its non-AI foundry business fails to generate sufficient cash flow to service its 2026 bonds.

- By Q3 2028, the Taiwan Financial Supervisory Commission will impose stricter loan-to-value limits on tech sector lending to prevent systemic risk from the debt overhang.

- Q1 2024AI chip demand begins to outstrip supply

Nvidia and AMD report record AI chip orders, triggering a capacity race among Taiwanese foundries.

- Q3 2025Taiwanese tech bond yields rise 50 bps

Lenders start demanding higher coupons as borrowing accelerates, according to Bloomberg data.

- Q1 2026TSMC issues $6B in bonds for AI packaging

The largest single debt issuance by a Taiwanese tech firm, earmarked for CoWoS and 3nm capacity.

- May 2026Total debt deals hit record $14.5B

Bloomberg reports the highest-ever annualized borrowing by Taiwanese tech firms, driven by AI demand.

- Q2 2028 (predicted)AI capex cycle peaks

Historical semiconductor cycles suggest a peak in AI infrastructure investment, leading to overcapacity and debt stress.

Taiwanese Tech Debt Issuance by Company (2026 est.)

- The $14.5 billion debt record is not a sign of strength but a race to lock in financing before rates rise further.

- TSMC is the only Taiwanese firm with truly low-risk debt; smaller players are paying a premium that will erode margins.

- The AI chip supply bottleneck will ease in H2 2026, but at the cost of a potential debt crisis in 2028.

- Institutional investors are the real winners — they are collecting 80 bps more yield on Taiwanese tech bonds than in 2024.

- Regulators in Taiwan are already concerned about bank concentration risk, which could lead to tighter lending rules by 2027.

Source and attribution

Bloomberg Technology

AI Boom Fuels Record $14.5 Billion in Taiwan Tech Firm Borrowing

Discussion

Add a comment